By Tanvi Prabhu and Saumya Agarwal

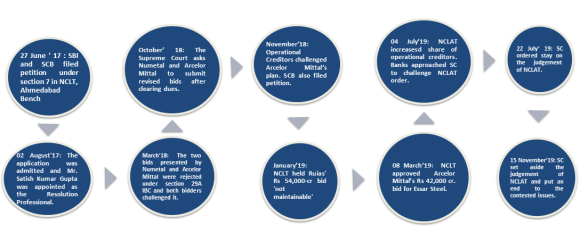

In Committee of Creditors of Essar Steel India Limited v. Satish Kumar Gupta &Ors, the Supreme Court on 15th November, 2019 dismissed the NCLAT order and upheld the approved Resolution Plan of ArcelorMittal in a joint venture with Japan’s Nippon Steel. It includes a payment of Rs. 42,000 cr. upfront towards resolution debt and further Rs. 8,000 cr. of capital infusion to support growth. The Plan provides for differential payment to secured and unsecured creditors, viz., State Bank of India (SBI) and other secured financial creditors to recover 92% of their admitted dues, approximately Rs. 13,000 cr., whilst Standard Chartered Bank (SCB) stands to recover 5% of approximately Rs. 3000 cr. Further, the operational creditors have been divided into two categories: small creditors with claims below Rs. 1 cr., who will be paid their dues in full and others in excess of Rs. 1 cr., who will collectively receive Rs. 1196 cr. out of admitted debt of Rs. 3339 cr. and individually receive liquidation value (a little more than nil in majority cases). The workmen and employees will be paid full dues amounting to Rs. 18 cr.

Key Takeaways:

- Commercial wisdom of the Committee of Creditors [“CoC”] held paramount to determine ‘feasibility and viability’ of a Plan taking into account all aspects of implementation including distribution of funds among various classes of creditors as held by the apex Court in Sashidhar v. Indian Overseas Bank[1] earlier. Majority vote (not less than 66% of voting share of Financial Creditors [“FCs”]) of the CoC to be the ultimate decision provided interests of all stakeholders are balanced simultaneously with asset value maximization.

- As embodied by the Code, different classes of creditors are to be given differential treatment. NCLAT order has been overturned by Apex Court, i.e. secured and unsecured FCs will not be treated equally and neither will operational creditors (OCs) nor FCs be at par. Distribution of funds will be as decided by CoC in accordance with the Plan as approved on 23.10.2018 submitted by ArcelorMittal and approved by NCLT Ahmedabad.

- Scope of judicial review to Adjudicating Authority [“NCLT”] is limited to four corners of section 31 read with section 30(2) of the Code, while that of Appellate Authority [“NCLAT”] is limited to section 32 read with section 61(3) i.e. to apply judicial mind without encroaching upon business decisions of the CoC. The task is to objectively satisfy itself ensuring compliance with existing laws in force based on reasoning provided by the CoC. In case of dissatisfaction, the Plan may be sent back to the CoC directing due compliance to parameters under Regulation 38 of CIRP Regulations before resubmission.

- Insolvency and Bankruptcy (Amendment) Act, 2019 has been held constitutionally valid concurring with the reasoning as given by the apex court in Swiss Ribbons & Ors. v. Union of India[2] (Swiss Ribbons), with regard to courts giving a certain degree of deference to legislative judgements in relation to economic choices. The word “mandatory” is to be deleted from section 4 of the amendment act so as to protect the interest of parties in case the delay beyond 330 days is due to the litigation.

- The Court reiterated that under section 31(1) all stakeholders, including guarantors would be bound by the CoC approved Plan. It further added that the guarantor’s right of subrogation (against Corporate Debtor (CD)) can be extinguished under the terms of the Plan.

- The functions of the Resolution Professional as encapsulated under the Insolvency and Bankruptcy Code, 2016 (Code) was asserted to be strictly administrative and non-adjudicatory.

- As decided by the Committee of Creditors (CoC) and consented to by ArcelorMittal in terms of Request for Proposal under section 25 of the Code, profits during the Corporate Insolvency Resolution Process (CIRP) will not go towards payment of debts to creditors.

- CoC is not barred from forming sub-committees for negotiation with resolution applicants or for any other administrative acts; provided, such acts are ratified by CoC, since, under section 28(1) (h) the powers of CoC cannot be delegated to any other person.

- The court clarified that the successful resolution applicant cannot be burdened with undecided claims at a later stage as it would hinder the acquisition of the corporate debtor.

Analysis – Two contentious points:

Treatment of OC and FC: Effective practical solution?

The Code clearly creates different classes of creditors providing for their differential treatment and the same has been correctly upheld. The Bankruptcy Laws Reform Committee Report of 2015 adequately justifies this classification; as also shown in Swiss Ribbons judgment pointing out the intelligible differentia between financial and operational debt and functions of creditors. The UNCITRAL Legislative Guide and the 2015 World Bank Report opine that these general principles of priority between secured/unsecured and financial/operational creditors are fundamental to credit efficiency.[3] Despite the Essar Steel judgment discussed herein, the question remains; will the safeguard of Section 30 of the Code and Regulation 38(1) of the CIRP regulations along with precedents such as Binani Cement[4] Resolution Plan serve the interests of OCs equitably?

A conflicting explanation is given in para 46 of the judgment stating that balancing of the interest of OCs will not be achieved by only granting the minimum amount under the Code i.e. liquidation value (which in many cases is nil) as that would not maximize the asset value of the CD. It directs that the CoC must have the commercial wisdom to arrive at an unbiased business decision that would pay off substantial dues of OCs. This indicates that mere semantic satisfaction of section 30(2) is not sufficient; rather the balancing spirit of the Code must be embodied in the approved Plan. However, the operative practical position demonstrated from the ArcelorMittal Plan (wherein majority OCs are recovering minimal dues compared to 92% recovery of dues by FCs) is that the business decision of CoC even if otherwise, cannot be trespassed by the Adjudicating Authority and satisfaction of section 30(2) is enough to consider the plan as being fair and equitable.

Though it is expected that by upholding the power of the CoC, this judgment will put to rest the question of funds distributed between OCs and FCs; in light of the above reasoning, only time will tell whether interests of OCs will be adequately addressed in the future, thus reducing further litigation upon this question. Notwithstanding the legal solution to the tussle between OCs and FCs, it is anticipated that in order to safeguard their interests, henceforth OCs will transform their service payment systems and change the way they deal with their client companies.

Guarantors: Without Redress?

The Code under section 31(1) clearly mentions that the approved Plan would be binding on all the stakeholders including the guarantors. As laid down in State Bank of India v.V. Ramakrishnan[5], Supreme Court held that the defence under section 133 of the Contract Act won’t be available on variation in debt under the Plan and it will be binding on guarantors. Similarly, in Lalit Mishra & Ors.v. Sharon Bio Medicine Ltd.[6], it was held that the right of subrogation under section 140 of the Contract Act would not be available to the guarantor under the code as the proceedings are not in the form of recovery but aim to maximise value of assets and the same was upheld by SC on appeal[7]. It has also been observed by the Insolvency Law Committee in its Report dated 26 March 2018, that assets of surety and corporate debtor are separate and that the defence of not being liable to pay any remaining amount once plan is approved cannot be taken. This view was recently dealt with by the NCLT, Principal Bench, New Delhi in the matter of Rave Scans Pvt. Ltd.[8] wherein the application filed by a guarantor challenging proceedings against him after approval of Plan was dismissed.

However, amidst this seemingly cemented position of law, came the case of IDBI Bank Ltd. v. EPC Constructions India Limited [9] wherein NCLT, Mumbai Bench in para 31 held that since the Plan expressly provides for extinguishment of guarantor’s right of subrogation pursuant to approval and hence guarantors would be liable to pay only if the approved plan expressly provided for such payment and not otherwise i.e. upon approval of the plan guarantors would be released from payment. The court further under para 32, termed the practice of payment of remaining dues by guarantors as a vicious circle and a never-ending process. However, the same was said assuming that the guarantors would then have the right of subrogation against the successful resolution applicant.

In our opinion, this conflicting position could not be settled by Essar Steel as here the right of subrogation is not being given. Moreover, it seems ironic that balance of all stakeholders is shown as being of paramount importance and yet the words “stakeholders including guarantors” have been used, they are effectively stuck between a rock and a hard place since they neither have the right of subrogation nor releases from payment.

The intention is to protect the creditors and to prevent the promoters from rewarding themselves. However, given the fact that the secured creditors are already being given a higher pedestal over others; it seems to be a valid point of contention as to why guarantors should not be released from the obligation of payment.

Practical issues:

- Logistical issue: Acquisition of the 10 million tonne steel plant located in Hazira, Surat, does not include the adjacent port operated by Essar Bulk Terminal Ltd which earlier facilitated transport of raw materials and export of finished goods at a pricing advantage with myriad of privileges. Now, to stay competitive, ArcelorMittal may source its materials through the Adani group operated port 17 km away (but incur cost of transportation to and fro the plant) or; it may attempt to rework a favourable new long term contract with the Essar port (which will have higher negotiating power due to its location) or; it should acquire the port from the Essar Group.[10]

- Realistic business goals?: Upon acquisition, ArcelorMittal intends to double the plant output to 15 million tonnes and may make management personnel changes to implement new strategy for resurgence. Certain projections claim that steel demand will grow by 5-7% by 2020, but in the present economic slowdown, intertwined major sectors like automotive and construction among others are facing serious demand crunch thus reducing expectations of a speedy resurrection[11] and raising doubts on the achievability of these targets.

Conclusion:

Stating that the judgement did not deliver well even after 800+ days would be unfair. The apex court has done a commendable job by clarifying some major conflicting questions of law and standing the ground in support of the Code. However, certain pertinent questions continue to exist on grounds of liability of guarantor and disparity between OCs and FCs. Further, due to the present volatile market conditions, ArcelorMittal must set reasonable expectations and make well thought out strategic decisions in order to compete successfully in the Indian Steel Industry.

The authors are currently in their fourth year, pursuing their law degree from National Law Institute University (NLIU), Bhopal

[1] K. Sashidhar v. Indian Overseas Bank, 2019 SCCOnline SC 257.

[2] Swiss Ribbons & Ors. v. Union of India (2019) 4 SCC 17

[3] UNCITRAL, Legislative Guide on Insolvency Law (Jan, 5,2020, 10.27 pm), https://www.uncitral.org/pdf/english/texts/insolven/05-80722_Ebook.pdf

[4] Binani Industries Limited v. Bank of Baroda & Another, NCLAT Order dated Nov 22, 2018

[5] State Bank of India v. V. Ramakrishnan 2018 SCC OnLine SC 963.

[6] Lalit Mishra & Ors.v. Sharon Bio Medicine Ltd., Company Appeal (AT) (Insolvency) No. 164 of 2018 dated 19.12.2018.

[7] Lalit Mishra & Ors.v. Sharon Bio Medicine Ltd Civil Appeal No. 1603 of 2019.dated 05.04.2019.

[8] Rave Scans Pvt. Ltd., IB No. 01/2017, dated 09.05.2019

[9] IDBI Bank Ltd. v. EPC Constructions India Limited., MA 2738/2019 & MA 354/2019 in CP No.1832/IBC/NCLT/MB/MAH/2017 dated 20.09.2019

[10] P Manoj, Lakshmi Mittal faces a logistics challenge as he takes over Essar Steel, (Jan, 5,2020, 10.27 pm), https://www-thehindubusinessline-com.cdn.ampproject.org/c/s/www.thehindubusinessline.com/economy/logistics/lakshmi-mittal-to-take-overessarsteelsoon/article29993675.ece/amp/

[11]Business Line Bureau, ArcelorMittal to close Essar Steel deal by December-end, (Jan, 5,2020, 10.27 pm), https://www.thehindubusinessline.com/companies/arcelormittal-to-close-essar-steel-deal-by-december-end/article30014283.ece